Applied Nutrition

Summary

In a market often saturated with cash-burning consumer startups, Applied Nutrition stands out as a high-margin, vertically integrated powerhouse. From its humble beginnings as a local Liverpool supplements shop in 2014, the company has transformed into a global player, now exporting to over 85 countries.

The investment case is simple: Applied Nutrition is a founder-led business with a 44% three-year revenue and EBITDA CAGR, generating a 29% adjusted EBITDA margin. Unlike many competitors who outsource production, Applied Nutrition manufactures 80% of its sales in-house, giving it an “agile” advantage to capitalize on new trends like GLP-1 friendly nutrition and hydration sticks.

The Bottom Line: Applied Nutrition is a debt-free, highly cash-generative business positioned at the intersection of sports performance and the “everyday health” megatrend.

What They Sell

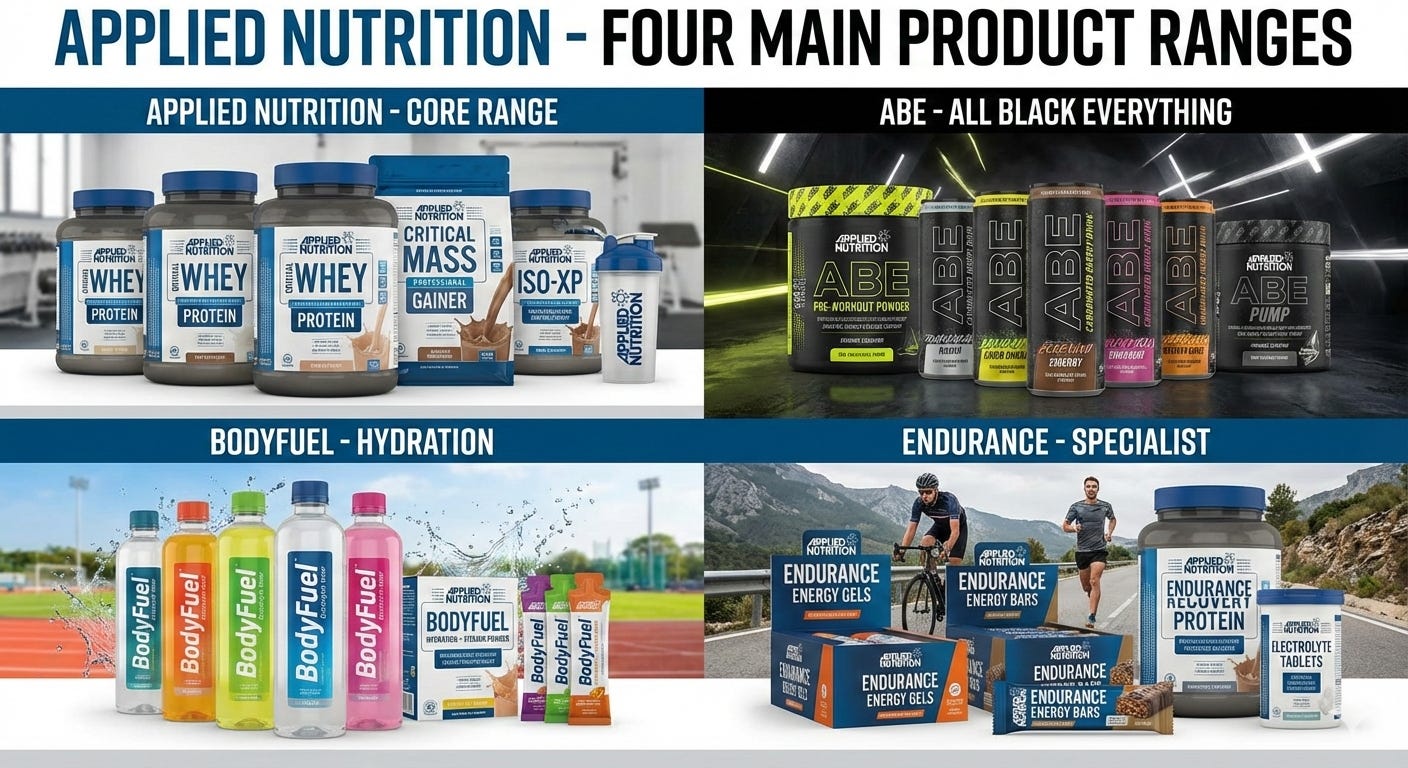

Applied Nutrition has successfully moved beyond its “hardcore” sports roots to capture a massive health and wellness demographic. They operate four distinct ranges:

Applied Nutrition (60% of revenue): The core wellness range including collagen and vitamins.

All Black Everything (ABE) (24% of revenue): A premium range for performance-focused gym-goers.

BodyFuel (8% of revenue): An entry-level hydration and price-conscious range.

Endurance (2% of revenue): Specialized products for runners and cyclists.

The Key Shift: Their customer base has diversified significantly. In just two years, the female demographic has doubled from 20% to 40% of their consumer base. This is no longer a niche brand; it is a mainstream lifestyle choice.

The Revenue Model: B2B Efficiency

Applied Nutrition utilizes a high-leverage B2B-first model, which accounts for 91% of total revenue. This allows the company to enter new markets with minimal capital expenditure by partnering with local distributors who provide local market expertise.

Retail Powerhouses: Their products are stocked in mainstream giants like Tesco, Asda, Morrisons, and Ocado in the UK, and Walmart, GNC, and Vitamin Shoppe in the US.

The Licensing “Free Lunch”: Recently, the company signed a three-year exclusive deal with Morrisons to launch 53 branded ready-meals. This deal requires zero capital expenditure from Applied Nutrition while significantly boosting brand awareness.

Vertical Integration: The Secret Sauce

The company’s most significant competitive edge is its 91,000 sq. ft. manufacturing facility in Knowsley, Liverpool. By controlling its own production, Applied Nutrition benefits from:

Superior Margins: While whey protein prices spiked 30% in FY25, the company maintained a robust 46% gross margin through agile formulation and pricing power.

Speed to Market: When a new trend emerges—such as the demand for creatine gummies or GLP-1 friendly protein for weight-loss drug users—the company can formulate and produce it in-house months before competitors can.

Efficiency: A recent factory extension increased revenue capacity to £200 million, allowing the company to scale without massive new overhead.

Growth Catalysts: The American Dream and Beyond

Applied Nutrition is currently in the early stages of a massive international rollout:

USA Expansion: The US business is still “in its infancy” but already has listings in HEB (Texas), Hy-Vee (Midwest), and GNC.

Latin America: A new agreement with one of the region’s largest distributors is opening doors in Mexico, Colombia, and Puerto Rico.

Structural Tailwinds: Over 80% of UK consumers now view supplements as a necessity rather than a luxury (including myself in this 80%).

Financials: Debt-Free and Cash-Rich

For a growth company, the balance sheet is exceptionally clean:

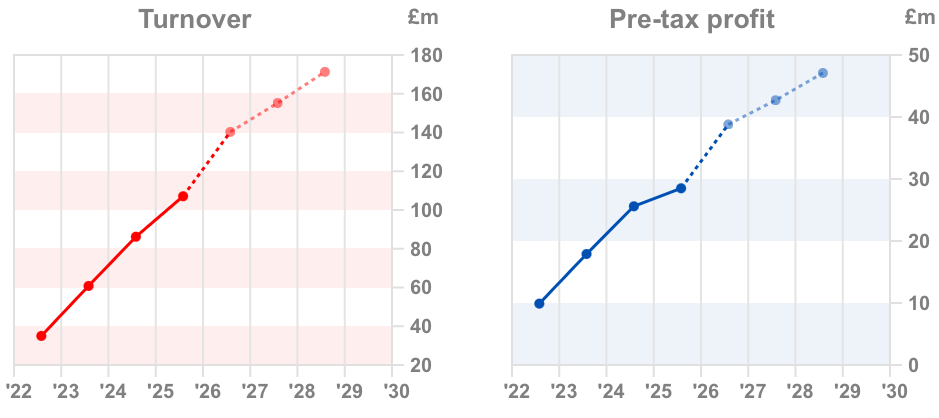

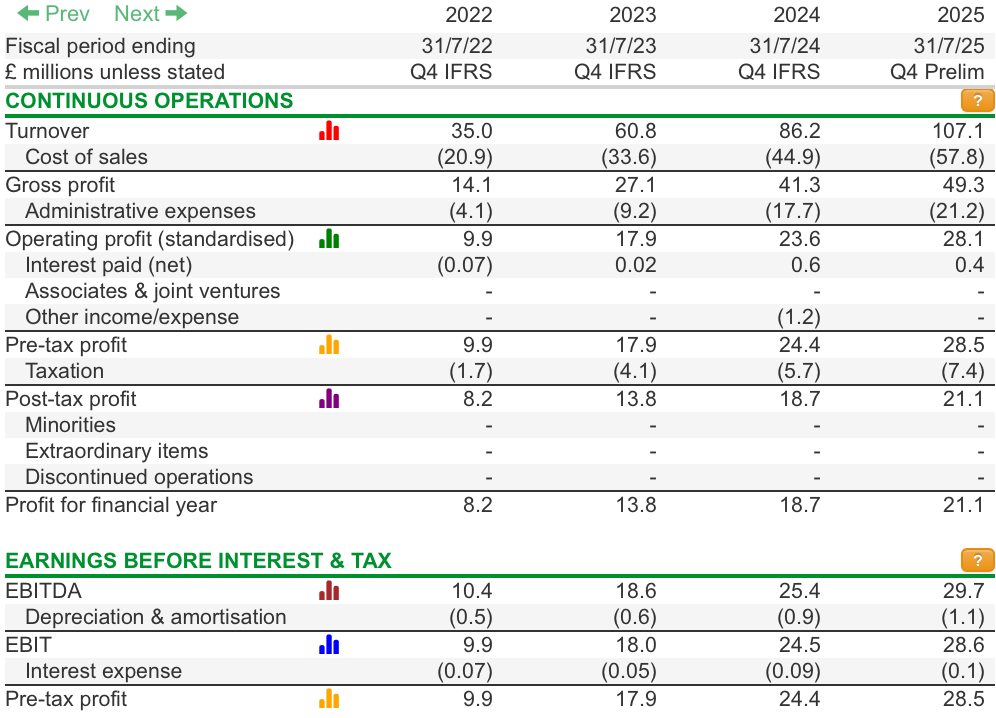

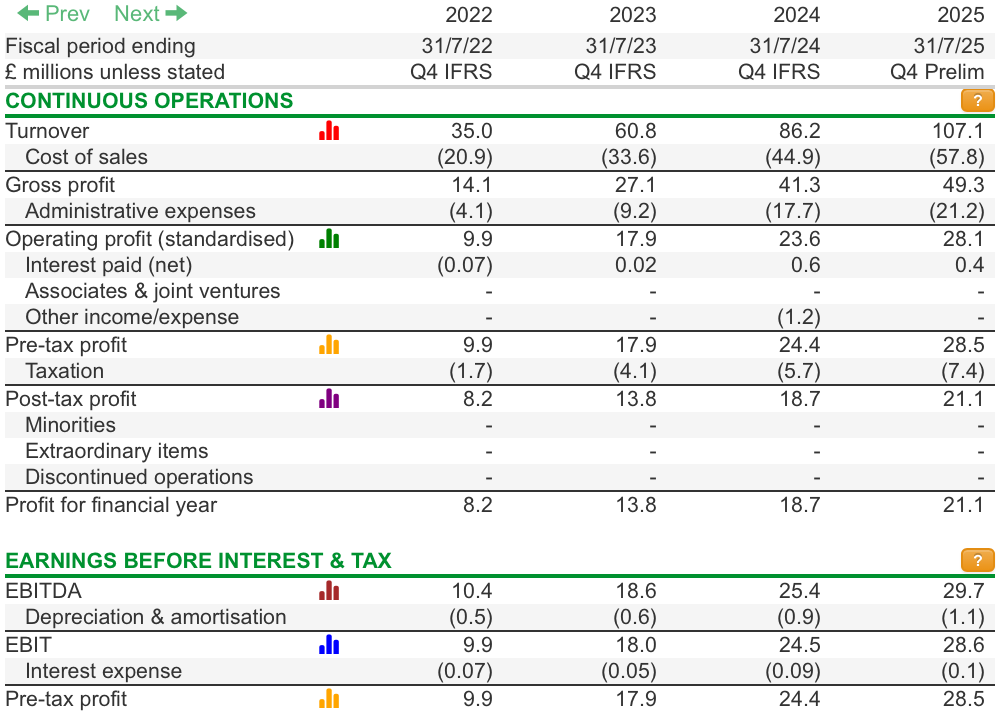

Revenue (FY25): £107.1m (+24.2%).

Free Cash Flow: £16.5m, representing a 72.4% conversion rate from adjusted profit after tax.

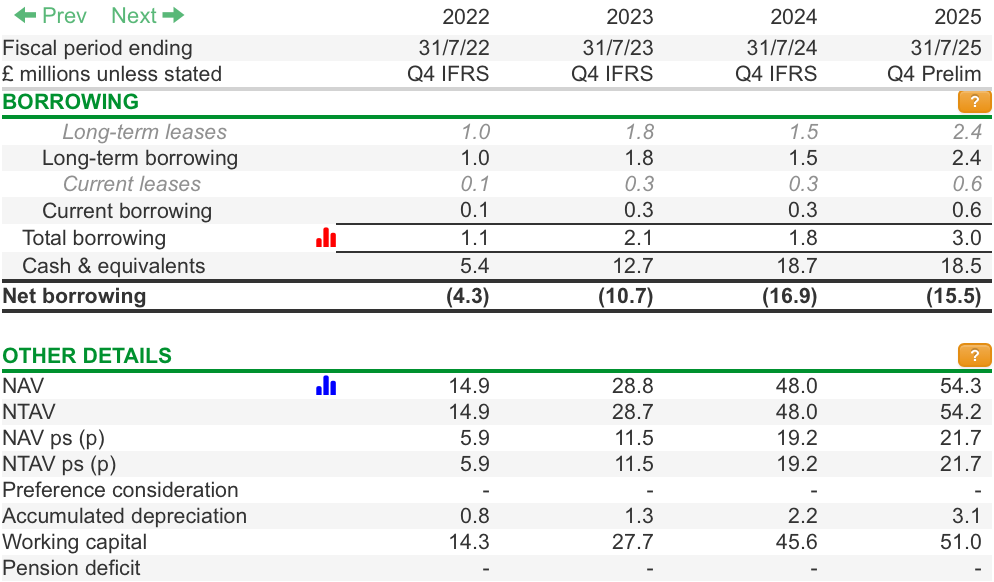

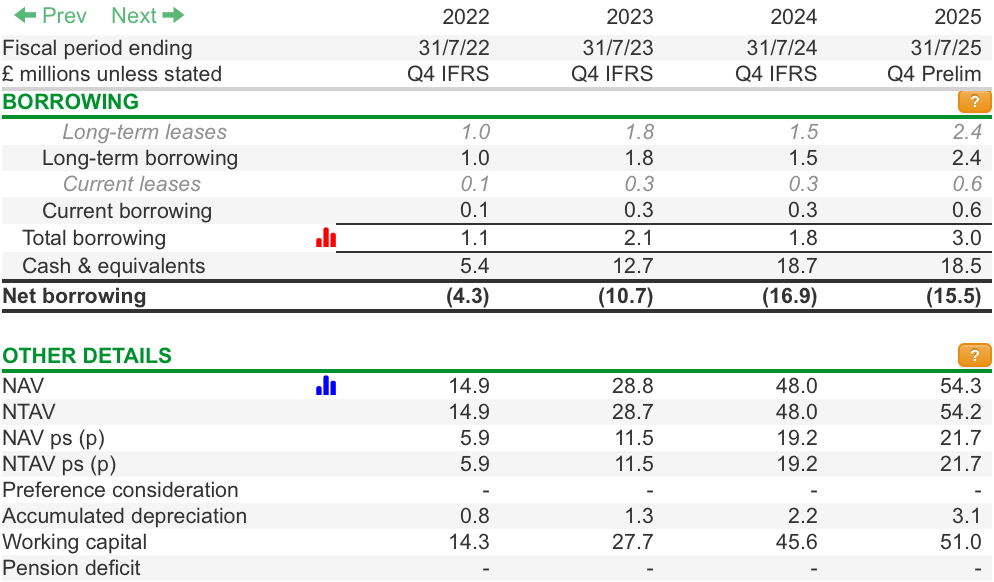

Net Cash: £18.5m at the end of the period, with zero debt.

Valuation

Applied Nutrition successfully listed on the London Stock Exchange in October 2024 at an offer price of 140p per share, resulting in an initial market capitalization of £350 million. Following a series of financial results that exceeded initial market expectations, the share price has appreciated to 256p, bringing the current market valuation to £640 million. Based on FY25 results, the company trades at a trailing Adjusted P/E of approximately 28.1x and an EV/Adjusted EBITDA multiple of 20.1x. This valuation reflects a growth premium justified by a 44% three-year CAGR for both revenue and adjusted EBITDA, supported by a global market opportunity projected to reach £279 billion by 2028. However, any misstep will very likely not being forgiven by the market, which can lead to a derating. We have to consider the sector’s competitiveness, therefore they can’t afford to lose any market share.

Shareholder Structure

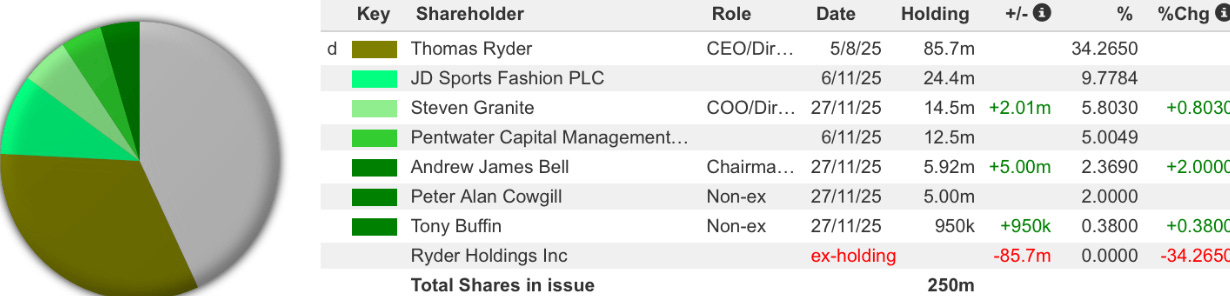

The shareholder register demonstrates strong alignment between management and investors, with Founder-CEO Thomas Ryder and COO Steven Granite collectively retaining a 40.06% stake in the 250 million shares in issue. Strategic backing is provided by JD Sports, which holds 9.77%, alongside institutional base including Pentwater Capital (5.00%).

Risks to Consider

Commodity Volatility: While the company is diversified, whey protein remains a key raw material vulnerable to price swings.

Single-Site Concentration: Almost all operations are based in Knowsley. Disruption there (fire, flood) would be a significant risk, though the company carries business interruption insurance.

Key Man Risk: Founder-CEO Thomas Ryder remains the visionary behind the brand. While a seasoned Board has been assembled post-IPO, his leadership is central to the culture.

Conclusion

Applied Nutrition represents a rare combination: hyper-growth combined with high profitability. The company has built a brand that resonates across demographics and a manufacturing engine that protects its margins. With the US expansion only just beginning and a high-margin licensing strategy kicking off in UK grocery, APN is a compelling story for investors seeking quality exposure to the global health and wellness boom.